Iran is building solar farms in its deserts. Germany is planting wind turbines in its seas. Both countries are racing to remake their electricity systems, spending billions in the process. The parallels are striking. The contrast in how they’re doing it says a lot about where each stands.

Two Crises, One Diagnosis

In January 2025, Iran shut down government offices and schools across multiple provinces. Rolling blackouts swept through Tehran, Isfahan, and the industrial heartland. Over 13 power plants had stopped running the previous month because there wasn’t enough gas to feed them. Peak electricity deficits approached 18 GW against a total demand of 77 GW, a shortfall of nearly a quarter.

The cause was a familiar story: decades of underinvestment in generation, transmission losses bleeding power from the grid, and a thermal fleet operating below 40% efficiency. Over 90% of Iran’s electricity still comes from burning fossil fuels. The country’s renewable share sits below 1%, one of the lowest in the region.

Germany’s crisis arrived differently. When Russian gas stopped flowing in 2022, the country faced the prospect of winter blackouts for the first time in decades. The Energiewende, Germany’s decades-long shift to renewables, suddenly looked less like a green vanity project and more like a survival strategy. The response was decisive: a coal phase-out by 2030, a legally binding requirement for 80% renewable electricity by the same year, and 100% by 2035.

Both countries arrived at the same conclusion from different directions. Fossil fuels are no longer reliable. Renewables are no longer optional.

Iran’s Solar Gamble

Iran sits on one of the world’s best solar belts. Global horizontal irradiance averages 5.3 kWh per square metre per day across the country’s arid central plateau, comparable to the Mojave Desert and ahead of southern Spain. The resource is enormous. The installed base was not.

Until recently, that is. The Renewable Energy and Energy Efficiency Organization (SATBA) reports that Iran’s total renewable capacity surpassed 4,500 MW by late April 2026, up from roughly 1,230 MW when the current administration took office. Around 1,200 MW came online in the final months of 2025 alone, even as military strikes hit parts of the country. Construction didn’t stop.

The scale of ambition has grown with it. In March 2025, SATBA announced that permits had been issued for 29,000 MW of solar power capacity. By December, that figure had been revised to 100,000 MW. Not all of it will get built, at least not quickly. Permits are one thing; financing, grid connection, and procurement are another. But the signalling is clear.

The money is starting to move. The National Development Fund, Iran’s sovereign wealth fund, has committed to building 15,000 MW of solar and wind capacity across two national projects. The larger of these, a 7,000 MW solar programme, carries a total investment estimate of $2.3 billion, of which $1 billion has already been disbursed to SATBA. An additional $461 million has been introduced to broker banks for civil partnership contracts with the private sector.

Then there is MAPNA Group, Iran’s largest engineering and construction conglomerate. In March 2026, MAPNA announced a standalone 1 GW solar expansion, estimated at $800 million to $1 billion, integrating its proprietary energy storage and grid-stabilisation systems. The project would more than triple Iran’s operational solar capacity in one build.

At roughly $329 per kilowatt for the NDF programme and $800-1,000 per kilowatt for MAPNA’s project, Iran’s solar costs sit above the global utility-scale average of $691/kW reported by IRENA for 2024. Sanctions, import premiums on panels and inverters, and higher financing costs all contribute to the gap. Even so, with Iran’s irradiance levels pushing capacity factors to 18-22%, the levelised cost of electricity remains competitive, particularly against the cost of diesel backup generators that many Iranian businesses and households already rely on.

The power shortages are the immediate driver. But there is a longer-term logic. Iran’s policymakers have set a target of 10% renewable electricity by 2025 and 30% by 2030, with 50 GW of total renewable capacity by 2031. These are ambitious numbers for a country where solar panels on homes were rare five years ago.

Germany’s Offshore Colossus

If Iran’s renewable story is about catching up fast, Germany’s is about scaling up from an already massive base.

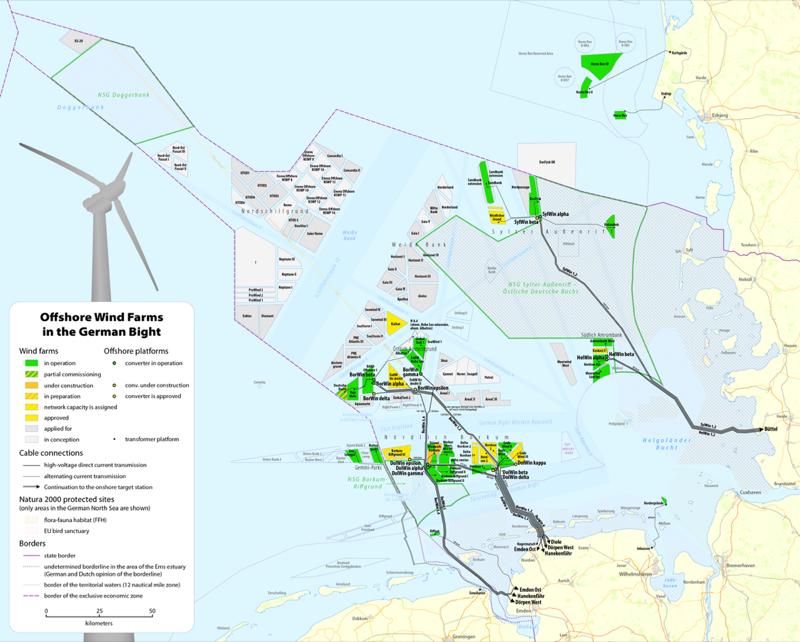

As of mid-2025, 1,639 offshore wind turbines with a combined capacity of 9.2 GW dot the North and Baltic Seas. They generated 26.1 TWh of electricity in 2025, around 10% more than the year before. That is enough to power roughly 7.5 million German homes.

The trajectory from here is steep. The Wind Energy at Sea Act (WindSeeG) mandates 30 GW of offshore wind by 2030, 40 GW by 2035, and 70 GW by 2045. A political agreement between federal and state governments in 2022 pushed the 2035 target to 50 GW. The Flächenentwicklungsplan (FEP) 2025, published by the Federal Maritime and Hydrographic Agency (BSH) in January 2025, maps out the sites and grid connections needed to get there, with specifications running through 2034. A further update is planned for 2025 to cover longer-term targets.

Getting the power from the turbines to the mainland is a multi-billion-euro engineering challenge in its own right.

Each 2 GW HVDC connection, the standard unit of offshore grid expansion, costs between EUR 2.5 and 3.0 billion. That covers the offshore converter platform, subsea cables, and onshore converter station. TenneT, the dominant transmission system operator for the North Sea, plans 12 GW of offshore grid capacity by 2032 and is investing over EUR 40 billion in offshore expansion by 2031. In April 2023, TenneT awarded EUR 23 billion in HVDC contracts to Siemens Energy and GE Vernova for projects including BalWin4 and LanWin1.

In the Baltic Sea, 50Hertz is breaking new ground. Its Ostwind 4 project, awarded to a GE Vernova and Drydocks World consortium in December 2024, will be the first 2 GW/525-kV HVDC system in the German Baltic Sea. A 110 km subsea cable will run from an offshore converter platform northeast of Rügen island to Lubmin on the mainland. The technology can transport more power at lower losses than the alternating-current connections used in the Baltic to date.

The wind farm concession area for Ostwind 4 was purchased at auction by TotalEnergies. The French energy giant bid EUR 1.305 million per MW for the site. Offshore wind strike prices in Germany have fallen roughly 60% over the past decade, with some North Sea sites attracting zero-subsidy bids. The LCOE for new offshore wind in Germany now sits at EUR 55-103/MWh, according to Ember’s 2025 analysis.

Private capital is following. RWE, EnBW, Ørsted, and TotalEnergies have all made final investment decisions on major North Sea projects in 2024 and 2025. The Nordlicht I and II projects, which together represent several gigawatts, received FIDs in spring 2025. A Hamburg summit in early 2026 outlined plans to mobilise up to one trillion euros between 2031 and 2040, installing up to 15 GW per year.

The Financial Reality Check

Side by side, the numbers reveal how differently these two programmes are structured.

Iran’s 7,000 MW solar programme carries a $2.3 billion price tag, or roughly $329 per kilowatt. MAPNA’s 1 GW project comes in at $800-1,000/kW. For comparison, the global average for utility-scale solar in 2024 was $691/kW, according to IRENA. Iran pays a premium for being cut off from the most competitive supply chains.

Germany’s offshore programme is in a different financial universe. Each 2 GW grid connection alone costs EUR 2.5-3 billion, and that is before the wind turbines themselves. Total offshore grid investment through 2037 will exceed EUR 100 billion. Add the cost of the wind farms, installation vessels, maintenance, and the onshore transmission upgrades needed to carry the power south, and the programme becomes one of the largest infrastructure investments in European history.

The LCOE comparison is equally stark. Solar PV in Iran, even at elevated capital costs, produces electricity at an estimated $0.03-0.05/kWh thanks to the country’s exceptional irradiance. Germany’s offshore wind comes in at EUR 0.055-0.103/kWh. Both are competitive with fossil fuel generation in their respective contexts. But the capital intensity per kilowatt-hour is radically different.

Germany’s advantage lies in its ability to mobilise capital at scale. TenneT invested EUR 10.6 billion in 2024 alone across onshore and offshore grid expansion. Germany’s renewable energy sector benefits from deep, liquid capital markets, EU structural funds, the European Investment Bank, and a regulatory framework that gives investors long-term revenue certainty through feed-in tariffs and auction mechanisms.

Iran’s programme, by contrast, relies on the National Development Fund, state-directed bank lending, and a small but growing private sector. The $2.3 billion committed to the 7,000 MW programme is significant by Iranian standards but modest compared to what Germany spends annually on a single transmission corridor. Sanctions restrict access to international project finance, multilateral lenders, and the most cost-competitive equipment suppliers.

The European Connection

This is where the IranEU angle becomes unavoidable.

European companies are already embedded in Germany’s offshore programme. Siemens Energy builds the converter stations for TenneT’s North Sea grid connections. GE Vernova, which has major operations in Germany including a new HVDC Competence Center in Berlin, is supplying the technology for Ostwind 4 in the Baltic Sea. NKT, the Danish cable manufacturer, is laying the subsea cables. TotalEnergies, a French company, won the concession for the wind farm area connected to Ostwind 4.

These are exactly the kinds of companies that, under different circumstances, could be supplying Iran’s solar sector. Europe’s solar engineering firms, grid technology providers, and project finance institutions have the expertise Iran needs. Siemens Energy, which exited the Iranian market under US pressure, built some of Iran’s most important power infrastructure in the 1990s and 2000s. The institutional knowledge still exists.

Instead, China is filling the gap. Chinese solar panel exports surged to record levels in March 2026, driven in part by demand from countries scrambling for alternatives to Middle Eastern fossil fuels after the Strait of Hormuz disruption. Iran is a natural destination. Chinese manufacturers already dominate the global PV supply chain, and sanctions give them a captive market with less competition.

The irony is layered. European sanctions on Iran push Tehran toward Chinese suppliers. The same Iran war that is accelerating Europe’s own renewable buildout is also boosting China’s clean-tech dominance. A Washington Post report from April 2026 noted that sales of Chinese electric vehicles and solar panels have surged since the start of the conflict. Reuters reported that Chinese clean-tech exporters posted record sales in March 2026 as oil and gas supplies from the Middle East were disrupted.

What Both Programmes Need

Despite their different scales and contexts, Iran and Germany face overlapping challenges.

Grid infrastructure is the shared bottleneck. Iran’s transmission network loses significant power to technical inefficiencies and inadequate interconnections. SATBA and Tavanir, the national grid operator, are exploring policies to modernise the system, but legislative support and funding remain works in progress. Germany’s north-south transmission corridors, projects like SuedLink, face permitting delays and local opposition even as billions in offshore investment hang on their timely completion.

Energy storage is another common need. MAPNA is integrating storage into its solar projects, recognising that solar without storage cannot replace dispatchable thermal generation. Germany’s NEP 2037/2045 explicitly models the role of battery storage, flexible loads, and electrolysers in absorbing variable renewable output. Both countries are learning that building generation capacity is only half the problem.

Workforce and supply chain constraints bind them too. Germany’s offshore wind sector faces a shortage of specialised vessels, port capacity, and skilled labour. Iran’s solar sector must import most of its equipment and train a workforce for an industry that barely existed a decade ago.

The Bottom Line

Iran is spending roughly $2-3 billion to add several gigawatts of solar capacity in its deserts, driven by an immediate electricity crisis and a government that has finally made renewables a priority. Germany is committing hundreds of billions to build an offshore wind empire in its seas, driven by a strategic decision to eliminate fossil fuel dependence entirely.

Both programmes are rational responses to genuine energy security problems. Both would benefit from technology transfer, shared engineering expertise, and cross-border investment. The Netzentwicklungsplan and the Flächenentwicklungsplan are marvels of coordinated planning that Iran’s energy bureaucracy could learn from. Iran’s solar irradiance and low land costs offer a resource advantage that German engineers can only dream of.

Sanctions ensure these two parallel universes never intersect. European companies build the grid connections that will carry German offshore wind to Berlin and Hamburg. Chinese companies supply the panels that will power Iranian homes and factories. The energy transition, like so much else in the EU-Iran relationship, proceeds in parallel but never together.

The cost of that separation is not abstract. It shows up in higher prices for Iranian consumers, slower deployment for both programmes, and a renewable supply chain that grows more Chinese-dominated by the month. When the political conditions eventually change, the companies that have spent a decade building Germany’s offshore infrastructure will find a solar market in Iran that has grown without them. The question is whether anyone in Berlin or Brussels will have noticed.