The World Has Plenty of Oil. It’s Running Out of the Fuels That Actually Matter.

Global crude oil inventories still sit at a comfortable 101 days of demand. That number has been cited repeatedly in recent weeks to argue that the world is handling the Strait of Hormuz disruption just fine. Goldman Sachs disagrees with the optimism, and their reasoning is worth paying attention to.

In a research note published on May 5, Goldman Sachs warned that while crude stocks remain above critical levels, the refined products the global economy actually runs on are depleting at a dangerous pace. Global commercial refined product stocks have dropped to roughly 45 days of demand, down from around 50 before the Hormuz disruption began. The gap between crude abundance and fuel scarcity is widening, and the consequences are already visible.

What’s Actually Running Short

The shortages are not evenly distributed across all fuel types. Three product categories stand out in Goldman’s analysis: jet fuel, naphtha, and liquefied petroleum gas (LPG).

Jet fuel is the most politically sensitive of the bunch. Goldman estimates that Europe’s commercial jet fuel inventories will dip below the International Energy Agency’s critical 23-day shortage threshold in June. The United Kingdom, which imports a large share of its jet fuel, faces the highest risk of rationing. Claudio Galimberti, chief economist at Rystad Energy, put it bluntly to Fortune: “We’re still kind of sleepwalking into this approaching disaster.” ARA (Amsterdam-Rotterdam-Antwerp) jet fuel stocks are already down 50% since late February, and the decline shows no sign of flattening.

Lufthansa has already cancelled 20,000 flights through October and warned that the Hormuz closure will add roughly $2 billion to its fuel costs. Airfares across Europe have jumped 20% or more year-on-year. Spain’s Volotea has even applied fuel surcharges retroactively to tickets already purchased.

Naphtha, a petrochemical feedstock used to produce plastics and industrial chemicals, tells an equally stark story. Inventories at the UAE’s Fujairah storage hub have crashed 72%, while northwest Europe’s ARA hub has seen a 37% decline since late February. This is not a marginal draw. It is a structural squeeze on the feedstocks that European chemical and plastics industries depend on.

LPG, used in heating, cooking, and chemical manufacturing, is tightening alongside both. Pakistan has already issued emergency LNG tenders as a power crisis deepens, a preview of the kind of cascading shortages that become visible when refined product buffers thin out.

The Refining Bottleneck

The paradox of the current crisis is straightforward: the world is not short of oil, but it is short of the capacity to turn that oil into the specific fuels the economy needs.

Refineries are not infinitely flexible machines. A typical European refinery produces jet fuel as roughly 10% of its total output, with the bulk going to gasoline and diesel. When jet fuel demand surges or supply chains get disrupted, refiners cannot simply flip a switch and double their kerosene yield.

TotalEnergies CEO Patrick Pouyanné told investors last week that the instruction to all European refineries is “max jet first.” BP and Austria’s OMV echoed similar messages. But the reality is incremental: a refinery might push jet fuel output from 10% to 13% of its production mix. Meaningful, but far from sufficient to offset the volumes normally flowing through the Strait of Hormuz.

Europe’s refining capacity has also been shrinking for years. Plants have closed, and the continent has grown increasingly dependent on imports of refined products from the Middle East and Asia-Pacific. Those imports are now the very flows being disrupted.

There is another technical constraint that rarely gets discussed. Many fuel storage tanks use floating roofs that move with the liquid surface to reduce evaporation and emissions. Those roofs cannot descend below roughly 20% of tank capacity without risking structural collapse. This means the usable volume in a storage tank is not 100% of its stated capacity; it is closer to 80%. When headline inventory numbers look low, the actual operational buffer is even thinner than it appears.

The War Europe Helped Make, and the Bill It’s Now Paying

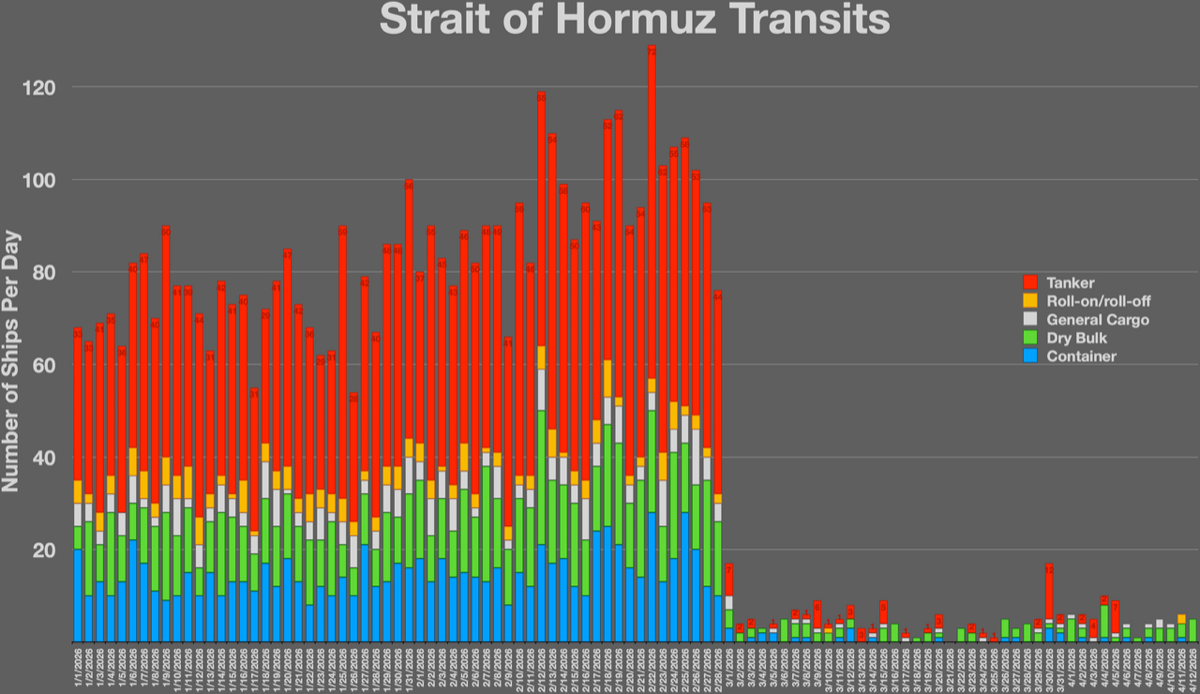

The Strait of Hormuz is not closed because of a natural disaster or a market failure. It is closed because the United States attacked Iran, and Europe, rather than trying to restrain its ally or pursue its own interests, spent years helping Washington build the pressure campaign that led to this outcome.

The pattern is not new. The EU signed up for every round of Iran sanctions, helped construct the compliance architecture that cut European companies out of one of the Middle East’s largest economies, and did so even when those sanctions served American strategic objectives more clearly than European ones. TotalEnergies was pushed out of Iran’s South Pars gas field. Eni lost years of upstream investment. Siemens was forced to wind down its role in Iran’s power infrastructure. European companies did not leave because the business case disappeared. They left because Washington told them to, and Brussels went along.

The JCPOA snapback, which Europe failed to prevent, has locked the Continent out of Iranian energy markets for a generation. But the real damage is not the lost revenue. It is the strategic dependency it created. By severing ties with Iran, Europe made itself more vulnerable to exactly the kind of supply shock it is now experiencing.

Now European airlines are grounding flights, petrochemical plants are watching feedstock stocks drain, and governments are scrambling for alternative fuel supplies. As we noted recently, a handful of traders are profiting from the volatility, but the broader European economy is absorbing the costs. The irony is that Europe helped build the pressure that contributed to the conflict, failed to use its diplomatic weight to prevent escalation, and is now bearing a disproportionate share of the economic fallout. That is not a sanctions regime working as intended. That is a policy failure compounding into a crisis.

The Countdown to Summer

Goldman Sachs identified several countries facing critical refined product supply levels: South Africa, India, Indonesia, Thailand, Taiwan, Malaysia, and Bangladesh. These are not marginal economies. They represent billions of consumers and significant industrial output.

Europe has a slightly better position because its remaining refineries can run harder on jet fuel, buying a few weeks of buffer. But Galimberti’s warning is clear: without a normalization of traffic through the Strait of Hormuz, Asia will face shortages first, and Europe’s additional runway will run out by late summer.

For travelers, the practical advice from analysts is straightforward. Book nonstop flights from major airports. Avoid secondary European hubs, particularly in southern Europe, which imports more heavily from the Middle East. Consider travel insurance. For businesses, the calculus is more complex: hedging fuel costs, auditing supply chains for petrochemical dependencies, and preparing for the possibility that fuel rationing could affect logistics well into autumn.

What Goldman’s Numbers Really Mean

Forty-five days of global refined product stocks is not a countdown to an apocalypse. It is a buffer, and buffers exist to be drawn down. The concern in Goldman’s analysis is not that the world runs out of fuel on day 46. It is that the rate of depletion is accelerating, that restocking depends on supply routes that are actively disrupted, and that the products running shortest are the ones with the fewest substitution options.

You can substitute natural gas for coal in a power plant. You cannot substitute anything for jet fuel in a turbofan engine. You cannot substitute anything for naphtha in a cracker producing ethylene. The specificity of these products is what makes their shortage so consequential, and it is why Goldman’s warning deserves more attention than the reassuring crude inventory headlines suggest.

The world has plenty of oil. It just cannot turn it into what it needs fast enough. And the reason Europe finds itself scrambling for fuel is not because of market forces or a sudden shift in global demand. It is because European policymakers chose to follow Washington’s Iran policy instead of their own, helped build the pressure that led to war, and now lack the supply relationships that might have softened the blow. Forty-five days of fuel is a reminder: when you help create a crisis, you don’t get to opt out of the consequences.